Your body count, screentime, followers on Tik Tok – all irrelevant numbers.

You know what truly matters? How much money you need to survive.

And budgeting can give you that number which arms you to make decisions about daily spending habits, your career, your time, and even your relationships.

Budgeting gives you a clear picture of your financial situation. This data on its own isn’t good or bad, and negative numbers don’t mean that you have failed. It only represents your [financial] reality, and the story you tell yourself about these numbers will shape your emotions and belief about your finances.

So, What is the 50/30/20 Rule?

The 50/30/20 Rule is a [rather inconsequential] rule that says that you could spend 50% of your income on your Needs, 30% on Wants, and 20% on your Savings. I say inconsequential because it is one of many ways to budget and view your finances. It’s not the end-all be-all but it is a helpful place to start budgeting.

According to this rule, you spend 50% on your Needs such as:

- Rent (utilities, wifi etc.)

- Car payment

- Car insurance

- Gas

- Phone service

Things you (or the item) might get hauled off for if you don’t pay for.

According to this rule, you spend 30% of your income on Wants. This might include:

- Eating out at restaraunts

- Online shopping

- A sweet treat

- Daily coffee

According to this rule, you spend 20% of your income on Savings. You might save in a:

- High yield savings account (HYSA)

- Roth IRA

- HSA

- SEP IRA etc.

Problems with the 50/30/20 Rule

What Belongs Where? (Is that a hard rule or…?)

Who determines if something is a need or a want? As someone who suffers from ADHD, is getting Chipotle after work a “want” or is it a need because your [lack of] executive function doesn’t allow you to cook sometimes? Deciphering what is a Need vs a Want changes from person to person.

Only 20% for savings?

Most financial experts recommend saving 10-15% for retirement.

However, if you don’t want to donate 45 years to work, you will definitely need WAY more than this. Considering that you’re young, you might want to shovel your income towards savings and investments due to compound interest since your expenses and responsibilities are relatively low compared to mid or end of career.

On top of this, this budgeting rule doesn’t explicitly create space for investment or debt payments.

Not suitable for very small or very large budgets

If you have a very small or very large income, this rule might not make sense for you. If you have a very small income, you won’t be able to fit all of your Needs. If your income is very large, you won’t need to spend so much on needs.

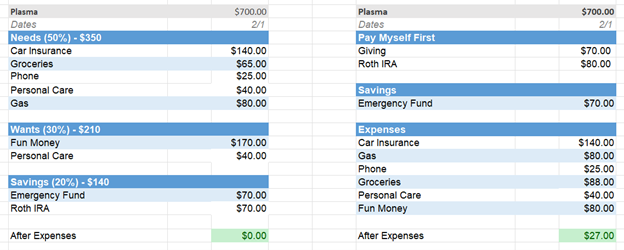

real world Example

For example, here is my college budget according to the 50/30/20 Rule:

In February 2023, I made $700.

On the left is my budget using the rule and on the right is my budget normally.

Key Differences

- I had to shrink my expenses to fit into my $350 limit meaning I cut important expenses like groceries

- My “Fun Money” budget doubled. My budget using this rule became exciting. I could have a lot of coffee hang outs and (sustainable, *cough*) online shopping sprees with this money whereas in the other budget, $80 per month was adequate but would not permit frequent sprees.

- I had to move Personal Care which includes trash bags and soap for my dorm, as well as shampoo, sunscreen, and hair products to wants. I would hardly call toothpaste a “Want” but that’s the only way it fit.

- I had to cut my Roth IRA by a few dollars, but not by much.

Benefits of the 50/30/20 Rule

Constraints and Something to Start With

If you’re new to budgeting, this rule gives you boundaries to stay within. It helps you plan your lifestyle within your budget and doesn’t allow you to go over (which could lead to debt).

30% is Very Generous

If you live in Georgia, and make $45,000, after taxes that’s $875 monthly for just Wants (eating out, travel, shopping etc.

And this amount only goes up if your income is higher. Do you need to spend that much or can that money go other places reasonably without compromising your [mental] health?

How to Implement the 50/30/20 Rule

- Find out your current income. If it changes, try averaging over the past 4 paychecks.

- Use this worksheet by Ally Bank that automatically does the math OR

- Multiply that number by 0.5 or 50% for your Needs

- Multiply that number by 0.3 or 30% for your Wants

- Multiply that number by 0.2 or 20% for your Savings

- Copy down your expenses on the template or on a sheet of paper or spreadsheet.

- Start with invariable expenses (meaning they don’t change). For example, rent, car insurance, and phone don’t change month-to-month.

- Next, list your variable expenses, one expenses that do change (or you have power to change) such as groceries, gas, and eating out. Look at your debit card or credit card statements to make estimates for these amounts. When in doubt, round up these numbers up for now to make sure you have all your bases covered.

Conclusion

Overall, the 50/30/20 Rule is a pretty great place to start learning how to budget. It gives you a framework and a place to learn how much you need to live and how much you want to live.

Just because it doesn’t leave space for you to save for retirement or pay off debt but it could save you a lot of stress putting it in your budget anyways. Bonus points if you put them into Needs (and treat them like a bill – well, loans are a bill lol)

Remember that in addition to this rule, there are also the Pay Yourself First method, Zero-based budgeting, and the infamous Envelope System. So, feel free to explore those methods if 50/30/20 isn’t for you.

No matter which budgeting style you try, by reading this you’re thinking and trying which is ACTION. Congrats to you. Think about your lifestyle. Your budget is not permanent, and you will probably spend too much. You didn’t die the other 3 years you were doing it and you won’t die today.